The first onchain product banks should launch.

For the past two years, the institutional conversation around blockchain has been dominated by stablecoins. Payment companies are experimenting with tokenized dollars. Regulators are publishing guidance. Banks are exploring faster settlement rails and programmable money. From an infrastructure perspective, the excitement is justified. Stablecoins are beginning to rewire how payments move globally.

From a business-to-business perspective, the value proposition is clear. Merchants want lower fees. Payment processors want faster settlement. Financial institutions want more efficient liquidity management. Stablecoins promise improvements across all of these dimensions.

But there is an important distinction between infrastructure innovation and consumer demand.

Most consumers do not care about payment infrastructure. When someone taps their phone at a checkout terminal, they are not thinking about consensus mechanisms, settlement layers, or transaction throughput. They want the payment to work instantly, reliably, and invisibly. The underlying rails are irrelevant. Whether a transaction settles through card networks, bank transfers, or a blockchain makes little difference to the person buying coffee.

This is why most payment revolutions are invisible to consumers. The migration from magnetic stripes to EMV chips, from cards to mobile wallets, or from batch settlement to real-time payments all occurred largely behind the scenes. The user experience barely changed.

Stablecoins are likely to follow the same path. They may dramatically improve merchant settlement and cross-border payments. They may reduce fees or increase speed for financial institutions. But as a consumer-facing product, they are unlikely to drive mass adoption on their own.

Banks sometimes forget this distinction. Financial infrastructure often evolves long before consumers even notice. So if stablecoins are not the product that will bring customers onchain, what is?

The answer is surprisingly simple in my opinion. Consumers want the ability to buy, sell, and hold digital assets through their bank.

Not because they care about blockchains or distributed ledgers, but because crypto has quietly become part of many people’s financial portfolios. Millions of users already hold digital assets through platforms like Coinbase, Robinhood, or PayPal. For them, crypto sits alongside stocks, savings accounts, and retirement funds as another category of wealth.

Once that shift happens, expectations change. Customers naturally ask a simple question: if their bank can provide access to equities, foreign exchange, or ETFs, why should digital assets be any different?

This is why Buy / Sell / Hold is the most natural starting point for banks exploring onchain finance. It does not require customers to understand blockchains. It does not change the way people interact with money. It simply extends the bank’s traditional role as custodian and investment gateway to a new asset class.

In other words, the path to onchain finance does not begin with reinventing payments. It begins with offering customers access to the assets they already want to own.

Digital assets are already part of the financial system

Digital assets have quietly crossed a threshold over the past few years. They are no longer an experiment sitting at the edges of finance, but they’re increasingly treated as a legitimate asset class. Institutional capital has accelerated this shift. Asset managers such as BlackRock and Fidelity Investments have launched spot Bitcoin ETFs, giving traditional investors regulated exposure to crypto markets. Public companies including MicroStrategy and Tesla have held Bitcoin on their balance sheets. Meanwhile, retail trading platforms such as Coinbase, Robinhood, and PayPal have made digital assets accessible to tens of millions of users.

Consumer adoption followed quickly. As of early 2026, approximately 30% of American adults, roughly 70.4 million people, own cryptocurrency, marking a slight increase from 27% in 2024, reports Security.org. Ownership is highest among men aged 18-49, and 61% of these holders plan to increase their investments in 2026. Among younger demographics, the proportion is even higher. What matters here is not the exact number. What matters is that digital assets have become part of many individuals’ financial portfolios. For a growing segment of customers, Bitcoin or Ethereum sits alongside stocks, savings accounts, and retirement funds as a standard component of personal wealth. Once that happens, expectations change.

If a bank can provide access to equities, foreign exchange, or commodities, why should it not provide access to digital assets as well?

Why “buy/sell/hold” should be the first use case

When banks begin exploring blockchain strategies, the conversation often jumps immediately to ambitious ideas: tokenized deposits, programmable payments, or entirely new settlement networks. These concepts may eventually reshape financial infrastructure, but they are not necessarily the most practical starting point. The first step should be far simpler: buy, sell, and hold digital assets.

In essence, this means allowing customers to purchase crypto through their bank, store it securely in custody, and convert it back to fiat when they choose. Conceptually, it is not a new business line at all. Banks have been offering access to financial markets for decades through brokerage services, foreign exchange desks, and commodity exposure. Digital assets are simply another asset class entering that universe.

For customers, the value proposition is straightforward. They want one trusted institution where they can manage their financial life: deposits, investments, credit products, and increasingly, digital assets. Fragmentation across multiple apps and platforms introduces friction, operational complexity, and risk. Consolidation remains one of the core advantages of banking.

Fintech platforms understood this early. A telling example is Revolut. The neobank introduced crypto trading in 2017, allowing users to buy, sell, and hold digital assets directly inside the app. The feature quickly became one of its most powerful growth drivers. Today, more than 14 million Revolut users actively trade crypto, representing roughly one-fifth of its global customer base. The impact went beyond trading revenue. Crypto helped strengthen Revolut’s position as a financial “super app,” contributing to rapid customer growth. The company added nearly 15 million new users in a single year, bringing its total user base to over 52 million customers globally.

The strategic lesson for banks is straightforward. Crypto does not need to replace the traditional financial system overnight to be disruptive, it simply needs to capture a portion of the customer relationship. Once assets sit inside a platform, the relationship deepens. Custody leads naturally to payments, lending, savings products, and portfolio management. Over time, the platform becomes the place where customers manage their financial lives. This is the strategic risk for banks.

If banks do not provide access to this new asset class, customers will inevitably seek it elsewhere. And when they do, the platform that holds those assets may gradually become the center of their financial life.

Banking has always been about custody

Banks are often described through the services they offer (payments, lending, investments, wealth management, etc.). But beneath all of these activities lies a simpler function: custody.

Banks have always been institutions of custody and trust. People deposit their money with the expectation that it will be secure, accessible, and professionally managed. Banking institutions exist primarily to safeguard assets and facilitate the transfer of value. Deposits, securities, and financial instruments are ultimately all forms of custody.

Crypto custody therefore does not represent a radical departure from banking, it’s a technological extension of the same fundamental role. The difference lies in what is being safeguarded. Instead of holding funds in accounts or securities in ledgers, digital asset custody involves securing cryptographic keys that control assets on a blockchain.

Control over those keys determines ownership of the associated funds. Lose the key and the asset is effectively lost. From a technological perspective, this shifts the challenge from account management to cryptographic key management. But banks are not strangers to cryptography. They have been managing encryption keys for decades in payment infrastructure, secure messaging, and hardware security modules. What has historically been missing is infrastructure capable of managing blockchain keys at institutional scale while maintaining regulatory compliance, operational governance, and security guarantees. That infrastructure is now emerging.

The move toward crypto custody and trading is existential. Within five years, the question won’t be whether banks offer digital asset services. The question will be which banks managed to adapt in time. The institutions moving early understand this. Crypto is not a threat to banking, it’s simply the next step in the long evolution of money and financial infrastructure. Banks that recognize this now are positioning themselves for the next chapter of finance.

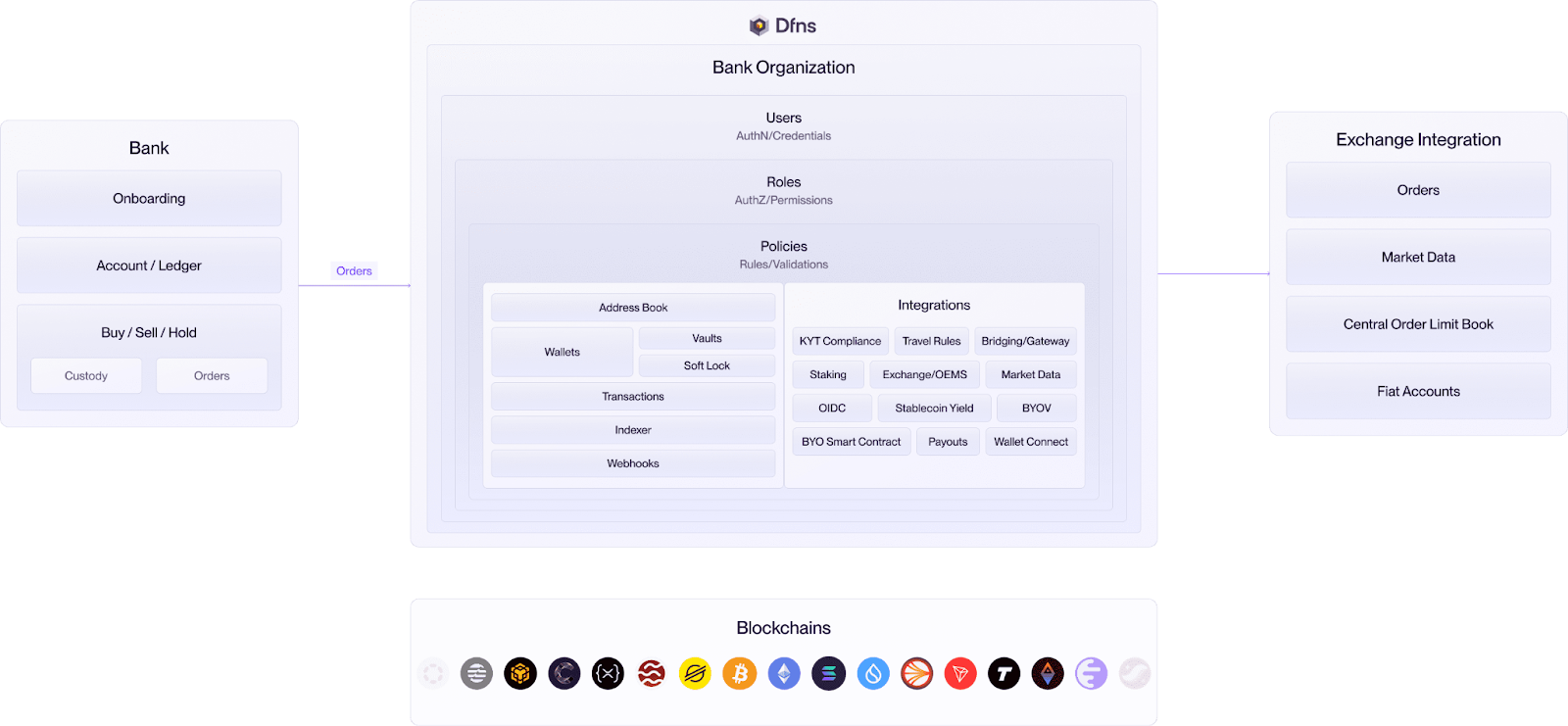

Dfns is the gateway infrastructure for “buy/sell/hold”

Launching a buy/sell/hold product looks deceptively simple from the outside. To the customer, it is just two buttons: buy and sell. Behind those actions, however, lies an entire operational stack that banks must operate with the same rigor they apply to payments, custody, and trading systems.

This is where the real challenge begins. A bank must be able to provision wallets for millions of users, secure cryptographic keys against internal and external threats, enforce governance and approval workflows, integrate liquidity venues for trading, and monitor transactions for compliance risks, all while maintaining the reliability and auditability expected from regulated financial infrastructure. Dfns was built precisely to solve this problem.

At its core, the platform provides institutional wallet infrastructure designed for financial institutions that need to operate digital asset services at scale. Customer wallets can be provisioned programmatically through APIs, allowing banks to create and manage digital asset accounts as easily as they manage traditional accounts today.

Security sits at the center of this architecture. Rather than storing private keys in a single location, Dfns uses distributed Multi-Party Computation (MPC) protocols to split cryptographic control across multiple secure environments. This removes the single point of failure that has historically plagued digital asset custody. No employee, system, or vendor can independently access customer funds. Every transaction requires coordinated cryptographic participation across the infrastructure.

For banks that prefer to retain direct control over custody hardware, Dfns also supports a bring-your-own-key (BYOK) model. Existing hardware security modules from providers such as IBM or Thales Group can be connected directly through PKCS#11-compatible interfaces. In this configuration, the cryptographic material remains inside the bank’s own infrastructure while Dfns provides the orchestration layer that governs transaction policies, workflows, and approvals.

Trading infrastructure is integrated into the same environment. Banks can connect to major liquidity venues and route buy and sell orders through established crypto markets. Once executed, assets settle directly into customer wallets managed by the bank. The process mirrors the operational logic of traditional brokerage systems, but with onchain settlement replacing traditional clearing infrastructure.

Compliance controls are embedded throughout this flow rather than added as an afterthought. Integrations with providers such as Chainalysis and Global Ledger allow institutions to screen transactions and monitor onchain activity before transfers reach the blockchain. Policies and approval workflows can be configured to reflect internal risk management frameworks and regulatory obligations.

The result is a fully operational custody and trading stack that can be integrated in weeks rather than years. More importantly, this infrastructure does not just enable buy/sell/hold. It establishes the foundational layer for onchain financial services inside the bank. Once wallets, trading connectivity, and compliance systems are in place, expanding into additional capabilities becomes far easier.

Deposits and withdrawals of digital assets become straightforward extensions of the same wallet infrastructure. Peer-to-peer transfers can operate across institutions. Cards can spend crypto balances directly. Lending, collateralization, and tokenized real-world assets can emerge on top of the same custody framework. This is why buy/sell/hold matters.

How to get started and roll out “buy/sell/hold”

Launching a buy/sell/hold product requires an operational stack that combines custody infrastructure, compliance controls, and market connectivity.

- Regulatory and Legal Compliance

- Determine what licenses are required to operate a digital asset business in your local jurisdiction.

- Ensure existing AML/KYC requirements and obligations are met.

- Assess regulatory classification of digital assets (commodity, security, payment token)

- Determine whether additional permissions are required (custody license, broker-dealer permissions, VASP registration, etc.)

- Implement Travel Rule compliance where applicable

- Define transaction monitoring and regulatory reporting obligations

- Risk Assessment

- Define the institution’s risk appetite and exposure limits

- Determine which assets to offer under the solution

- Decide whether deposits and withdrawals will be enabled at launch

- Define limits on customer exposure and transaction size

- Establish procedures to monitor suspicious activity

- Define asset listing criteria and liquidity thresholds

- Establish policies for forks, airdrops, chain upgrades, and network disruptions

- Define volatility management and market risk policies

- Custody Infrastructure

- Select a custody infrastructure capable of supporting regulatory and operational requirements

- Deploy wallet infrastructure capable of provisioning customer wallets at scale

- Secure private keys with the same rigor applied to critical payment infrastructure

- Implement multi-party computation (MPC) and/or FIPS 140-3 certified hardware security modules (HSMs)

- Ensure no single employee, system, or vendor can unilaterally access funds

- Define key lifecycle procedures (generation, rotation, backup, recovery)

- Implement disaster recovery and key restoration procedures

- Establish segregation of duties and cryptographic audit logging

- Exchange Venue

- Select one or multiple liquidity venues to ensure best price discovery

- Connect to exchanges or market makers capable of providing sufficient trading liquidity

- Route buy and sell orders through established crypto markets

- Ensure trades settle directly into customer wallets

- Integrate market data feeds and execution monitoring systems

- Define counterparty risk frameworks for trading venues and liquidity providers

- Operations and Settlement

- Establish fiat reserves at exchanges to facilitate crypto trading or adopt a daily settlement model

- Define reconciliation workflows between internal ledgers and blockchain balances

- Establish cost-basis and accounting methods for tax reporting

- Implement real-time reconciliation between internal accounting, exchange balances, and onchain wallets

- Define incident response procedures for failed or delayed blockchain transactions

- Define treasury management processes for managing liquidity across fiat and crypto

- Product Design

- Build a seamless user experience integrated into the bank’s digital channels

- Enable customers to easily buy, sell, and hold digital assets

- Provide portfolio visibility and transaction history

- Display transparent pricing, spreads, and execution confirmations

- Provide educational material and customer disclosures about digital assets

- Integrate crypto balances alongside traditional financial assets within the banking interface

Start with the obvious

The transition of finance to blockchain infrastructure will not happen all at once, and it will not begin with the most complex ideas. Historically, financial innovation rarely starts with entirely new behaviors. It starts by replicating familiar ones on new rails. That is precisely what the buy / sell / hold model represents.

It does not require consumers to understand blockchains, tokenization, or decentralized finance. It simply allows them to treat digital assets the same way they treat any other financial instrument: something they can purchase, store safely, and sell when they choose. In other words, it fits naturally within the mental model customers already have of banking and investing.

For banks, this simplicity is strategic. Launching a buy/sell/hold product forces the institution to build the core infrastructure required for the onchain economy: wallet provisioning, key custody, transaction governance, compliance monitoring, and connectivity to crypto markets. Once those components exist, they form a reusable foundation.

At that point, expanding into adjacent services becomes far more straightforward. Deposits and withdrawals are simply wallet transfers. Peer-to-peer payments become onchain movements of value. Cards can draw from crypto balances. Assets can be collateralized for loans. Lending markets, tokenized securities, and real-world assets can all plug into the same custody and settlement layer. In other words, buy/sell/hold is not the end state, it is the entry point.

Banks often approach blockchain as a distant transformation of financial infrastructure. But the institutions that succeed will likely be those that treat it as a gradual extension of services customers already expect. Start with a product that solves a real demand. Build the infrastructure behind it. Then expand. Finance is slowly but inevitably moving onchain. The banks that introduce a practical consumer use case today will not just participate in that shift, they will help shape how it unfolds.

Authors

Chris Sutton

As Chief Product Officer, Chris runs all things product and developer experience at Dfns. With a powerhouse background spanning Mastercard, Zerohash, IBM, Cisco, BlackRock, and Oasis Pro Markets, Chris has been at the edge of stablecoin payments, tokenized securities, and blockchain finance since 2016.

.jpg)